marginal revenue (MR) is the extra revenue that an additional unit of product will bring. It is the additional income from selling one more unit of a good; sometimes equal to price. It can also be described as the change in total revenue/change in number of units sold.

More formally, marginal revenue is equal to the change in total revenue over the change in quantity when the change in quantity is equal to one unit (or the change in output in the bracket where the change in revenue has occurred)

This can also be represented as a derivative. (Total revenue) = (Price Demanded) times (Quantity) or ![]() . Thus, by the product rule:

. Thus, by the product rule:

![]()

For a firm facing perfectly competitive markets, price does not change with quantity sold (![]() ), so marginal revenue is equal to price. For a monopoly, the price received will decline with quantity sold(

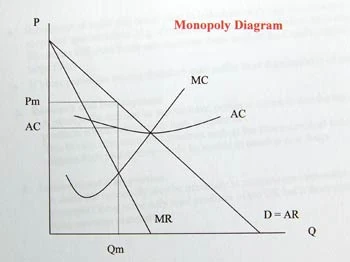

), so marginal revenue is equal to price. For a monopoly, the price received will decline with quantity sold(![]() ), so marginal revenue is less than price. This means that the profit-maximizing quantity, for which marginal revenue is equal to Marginal Cost (MC) will be lower for a monopoly than for a competitive firm, while the profit-maximizing price will be higher. When marginal revenue is positive, Price Elasticity of Demand [PED] is elastic, and when it is negative, PED is inelastic. When marginal revenue is equal to zero, price elasticity of demand is equal to 1.

), so marginal revenue is less than price. This means that the profit-maximizing quantity, for which marginal revenue is equal to Marginal Cost (MC) will be lower for a monopoly than for a competitive firm, while the profit-maximizing price will be higher. When marginal revenue is positive, Price Elasticity of Demand [PED] is elastic, and when it is negative, PED is inelastic. When marginal revenue is equal to zero, price elasticity of demand is equal to 1.

{kind=link}

Marginal Revenue seen here in a monopoly between the Y-axis and the demand curve.

Examples:

A promoter has properly estimated the demand curve for seats at an event to be

- Q = 40,000 − 2000P

where P is the price of a seat. The inverse demand curve, which determines price as a function of quantity, is therefore represented by

- P(Q) = 20 − Q / 2000

We therefore have

- T'R(Q) = 20Q − Q2 / 2000

Marginal revenue is the slope of total revenue

- M'R(Q) = 20 − Q / 1000