The theory of the firm is a set of economic theories that attempt to explain the nature of a firm, a company, and the firm's relationship to the marketplace. Theory of the firm is a higher level extension topic in the IB syllabus for microeconomics. Firms exist as an alternative system to the market mechanism when it is more efficient to produce in a non-price environment. For example, in a labor market, it might be very difficult or costly for firms or organisation to engage in production when they have to hire and fire their workers depending on demand/supply conditions. It might also be costly for employees to shift companies everyday looking for better alternatives. Thus, firms engage in a long-term contract with their employees to minimize the cost.

hCost Theory[]

• Fixed and Variable Costs

- A fixed cost is any cost that a firm has to pay to begin producing their good (i.e., the cost of capital). Variable costs are the costs that a firm needs to pay to continue with production of the good - these costs are usually land and labor.

- Primarily when talking about fixed and variable costs, we are talking about the short run. In the long run, everything is a variable cost because capital does not last forever - it depreciates with time and needs to be replaced or repaired eventually to continue with the production of the good. The distinction between a fixed cost and a variable cost must take the period of time into consideration.

- By definition, in the short run there is always at least one fixed cost. In the long run, all costs are variable.

• Total, average and marginal costs.

• Accounting cost + implicit opportunity cost = economic cost. Thus, economic profit is different from accounting profit in that to make an economic profit,

Short Run[]

• Total product, average product, marginal product.

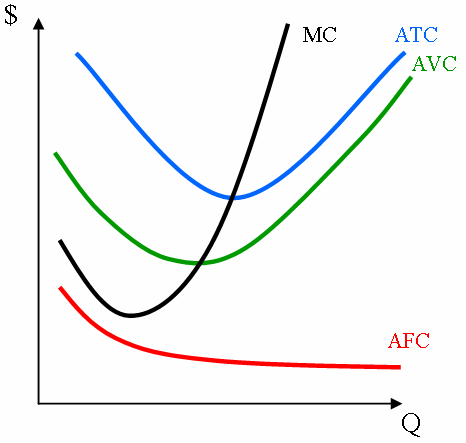

• Short-run cost curves:

{kind=link}

In the short-run, the costs of a firm are based on fixed costs and variable costs. The additional cost to make each quantity of a good is the marginal cost. The marginal cost curves intersects both the Average Variable Cost and Average Total Cost curves at the minimum points on the curves.

Long Run[]

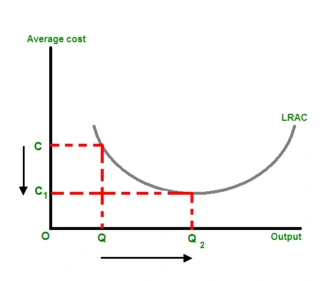

• Economies of scale - As the cost advantages that a business obtains due to expansion. They are factors that cause a producer’s average cost per unit to fall as scale is increased. Economies of scale is a long run concept and refers to reductions in unit cost as the size of a facility, or scale, increases.

{kind=link}

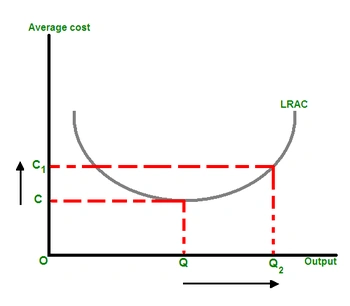

•Diseconomies of scale - are the forces that cause larger firms to produce goods and services at increased per-unit costs. These eventually counter economies and make it disadvantagous for a company to continually increase production.

{kind=link}

• Long-run cost curves

Revenues[]

Definition: The amount of money that a company actually receives during a specific period, including discounts and deductions for returned merchandise. It is the "top line" or "gross income" figure from which costs are subtracted to determine net income. Revenue is calculated by multiplying the price at which goods or services are sold by the number of units or amount sold. Revenue is also known as "REVs".

• Total revenue

Total money recived from the sale of any given quantity of output. In simplist terms, total revenue is price multiplied by quantity.

• Marginal revenue

Marginal revenue is the cost of producing an additional unit of that good, It reflects both changing average fixed costs and variable costs.

• Average revenue:

Average revenue is the average amount received from selling each unit; AR= TR/Q

Profit[]

Profit is the distinction between normal (zero) and supernormal (abnormal) profit.

- Normal (zero) profits are when a business uses resources and receives revenue in an amount that gives them a rate of return no different from the next best thing they could have done. A supernormal (abnormal) profit is when a business uses resources and receives revenue in an amount that gives them a rate of return higher than the next best thing.

- Profit maximization in terms of total revenue as well as the total costs, and in terms of marginal revenue and marginal cost.

- Profit maximization assumed to be the main goal of firms but other goals exist (sales volume maximization, revenue maximization, environmental concerns).

Efficiency[]

Productive efficiency is when the condition where the maximun output is produced with given resources and technology. That is, the lowest point on the average total cost curve. This is also where marginal cost is equal to average total cost by definition (MC = ATC). This is "efficient" because a firm is making exactly the right amount of goods so that it is spending the least amount of money to produce those goods. This is also the equilibrium level.

Allocative efficiency is when a firm is producing its optimal quantity of goods. This happens when its marginal cost curve is equal to its marginal revenue curve (MC = MR), or where the quantity supplied is equal to the quantity demanded (Qs = Qd). This is allocatively efficient because both producers and consumers are happy with the price and quantity demanded and there is no welfare loss due to too high or too low a price.

A firm can be both productively and allocatively efficient when the average total cost is equal to the marginal cost and marginal revenue (ATC=MC=MR). This occurs when a perfectly competitive market is at long run equilibrium, for example.

Perfect Competition[]

- These five criteria must be met in order for a market to have Perfect Competition.

1. All firms sell an identical product.

2. All firms are price takers.

3. All firms have a relatively small market share.

4. Buyers know the nature of the product being sold and the prices

charged by each firm.

5. The industry is characterized by freedom of entry and exit.

Monopoly[]

Profit maximizing level of output: In a monopoly, the firm can earn an abnormal profit when they set their prices according to the MC=MR condition. A monopoly has only 1 group that controls the whole market. Since the monopoly has no competition in the market, the demand will be satisfied by the firm. The single price monopolist thus sets the output at the profitmax point (MC=MR), the highest possible point on the demand curve.

For example, the U.S. Postal Service is a monopoly because they are in charge of all mail being sent in the United States.

Truly free market monopolies are very rare in reality. Most monopolies that do exist are government-created.

Monopolistic Competition[]

Efficiency in Monopolistic Competition: Like in the PCM, the monopolistically competitive firm earns a normal profit in the long run. However, a firm operating in monopolistic competition with other firms experiences subpar allocative efficiency (since MR is above marginal cost) and is not productively efficient since they produce at an average cost above ACmin. In short, the monopolistically competitive market is neither productively nor allocatively efficient, and the firm will not produce where P=MC.

Oligopoly[]

- A theory of market structure based on three assumptions: few sellers and many buyers, firms production either homogeneous of differentiated productions. An Oligopoly is about the same thing as a Monopoly, with the exception that at least two groups are controlling a market. ......

Price Discrimination[]

• Price Discrimination is when firms offers one (identical) good to different buyers at different prices (depending on the consumer's willingness to pay for it at a certain price).

• Reasons for price discrimination: The main and most obvious reason for price discrimination is that selling a good at different prices will serve to increase profits. A firm that has market power can increase profits by selling a good at the highest possible price that consumers are willing to pay. A firm can also use price discrimination to cut prices in order to force competitors out of the market or in order to penetrate a new market.

• Necessary conditions for the practice of price discrimination: To successfully price discriminate certain conditions must be met:

1) Company must be able to ID different groups of people.

2) Groups must have different demand curves.

3) Limited opportunities for arbitrage.

• Possible advantages to either the producer or the consumer.